Chains

BNB Beacon Chain

BNB ecosystem’s staking & governance layer

Staking

Earn rewards by securing the network

Build

Explore

Accelerate

Connect

The Next Step for Tokenized Equities: Funding Paths Matter After Assets Move Onchain

TL;DR

- Non-stablecoin RWA has passed $26B. BSC holds $4.257B of Ondo GM's $5.609B in cumulative DEX volume.

- BNB Chain has $17.9B in stablecoin supply and $4.0B in RWA value, with BUIDL, BENJI, and VBILL already providing institutional collateral access.

- The question has moved from issuing more tickers to whether those tickers can enter environments where capital already sits.

- xStocks and Ondo GM tokens look similar in a wallet but differ in structure and KYC rules, which matters once they enter DeFi.

Over the past year, the RWA conversation has moved from "can assets be put onchain?" to a more practical question: can onchain assets be used by a funding system that already exists?

That shift is visible across several asset types. Stablecoins are already the most mature form of dollar liquidity onchain. Tokenized Treasuries and tokenized money market funds are starting to sit closer to cash management and collateral. Tokenized commodities, private credit, fund interests, stocks, and ETFs are also expanding through different issuance and distribution paths.

According to RWA.xyz, in early May 2026, non-stablecoin RWA Distributed Asset Value had passed $26B, while Total Stablecoin Value was close to $300B. CoinGecko's 2026 RWA Report also noted that tokenized RWAs grew sharply from 2025 into Q1 2026. Tokenized Treasuries remained the main category, while activity in tokenized stocks, ETFs, and commodities also increased.

Against that backdrop, the important change in tokenized equities is the funding path. Stock and ETF exposure is starting to appear inside wallets, RWA dashboards, DEX routes, and CEX onchain entry points. A user may first see AAPLx, TSLAx, NVDAx, SPYx, or KWEBon, use stablecoins to gain exposure, and then hold those assets inside trading, collateral, or portfolio tools.

BNB Chain sits in this path as one of the infrastructure environments where several pieces are moving closer together: stablecoin capital, low cost trading, DEX and wallet access, RWA asset integration, collateral, and portfolio tools. According to the BNB Chain Institutional Finance page, when accessed on 2026-05-12, BNB Chain had $17.9B in stablecoin supply and $4.0B in RWA value. Those figures point to a dollar-denominated capital base that can be used by RWA and tokenized assets over time.

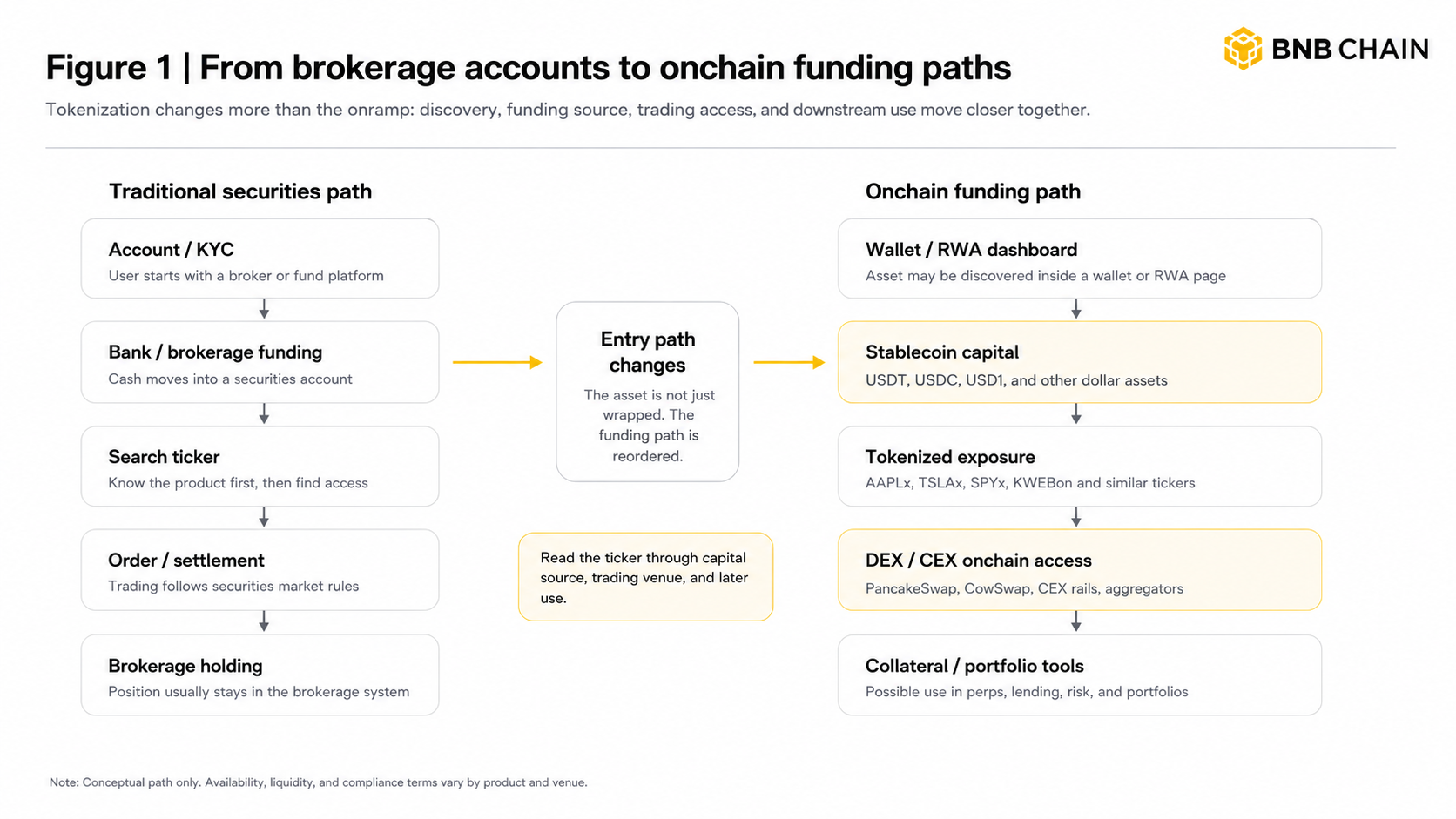

From brokerage accounts to wallet entry points

In the traditional path, stock and ETF exposure usually begins with a brokerage account. A user opens an account, completes KYC, funds the account, searches for a ticker, places an order, and waits for settlement. Asset discovery, funding, trading, and custody mostly stay inside the securities account system.

The onchain path works differently. A user may encounter a tokenized exposure first through a wallet, an RWA dashboard, a DEX route, or a CEX onchain deposit and withdrawal page. "Entry path" here means more than onramp. It covers asset discovery, source of funds, trading venue, and what the asset can be used for after it is held, including whether it can enter collateral or portfolio tools.

This is where tokenization and RWA become more than asset wrapping. They allow traditional asset exposure to connect with onchain funding, trading, and portfolio use. The relevant layers are asset discovery, funding source, trading venue, downstream use, and compliance. That structure applies regardless of which chain or provider is involved.

Figure 1: From brokerage accounts to onchain funding paths. Tokenization changes more than the onramp. It changes asset discovery, funding source, trading access, and downstream use.

KWEBon as a China Tech onchain sample

KWEBon is a clean sample of China Tech onchain, and it shows how asset discovery is changing.

KWEBon corresponds to an Ondo version of the KraneShares CSI China Internet ETF. KWEB tracks the CSI Overseas China Internet Index, covering Chinese internet companies listed on HKEX, NASDAQ, and NYSE. The KraneShares KWEB page showed about $6.91B in net assets on 2026-05-11. The five largest holdings were Alibaba, Tencent, PDD, Meituan, and NetEase.

In traditional finance, KWEB belongs to ETF allocation, China internet exposure, and cross-market index research. Once it enters Ondo Global Markets, it also gains an onchain discovery path. A user may first see KWEBon in a wallet or RWA page, then work backward to understand KWEB, the CSI Overseas China Internet Index, and the underlying constituents.

KWEBon is best read as an early sample. An asset that used to belong to the broker search box and ETF research workflow is starting to appear in wallet discovery and RWA dashboards.

This use case also sits next to the latest xStocks developments. In a 2026-04-30 announcement, xStocks had gone live on BNB Chain with 50+ tokenized US equities and ETFs, with 100+ more assets planned. Trading access includes PancakeSwap and CowSwap, with 1inch coming soon.

The competition is moving from "who can issue more tickers?" to "can these tickers enter the environment where users already hold capital, trade, and manage risk?"

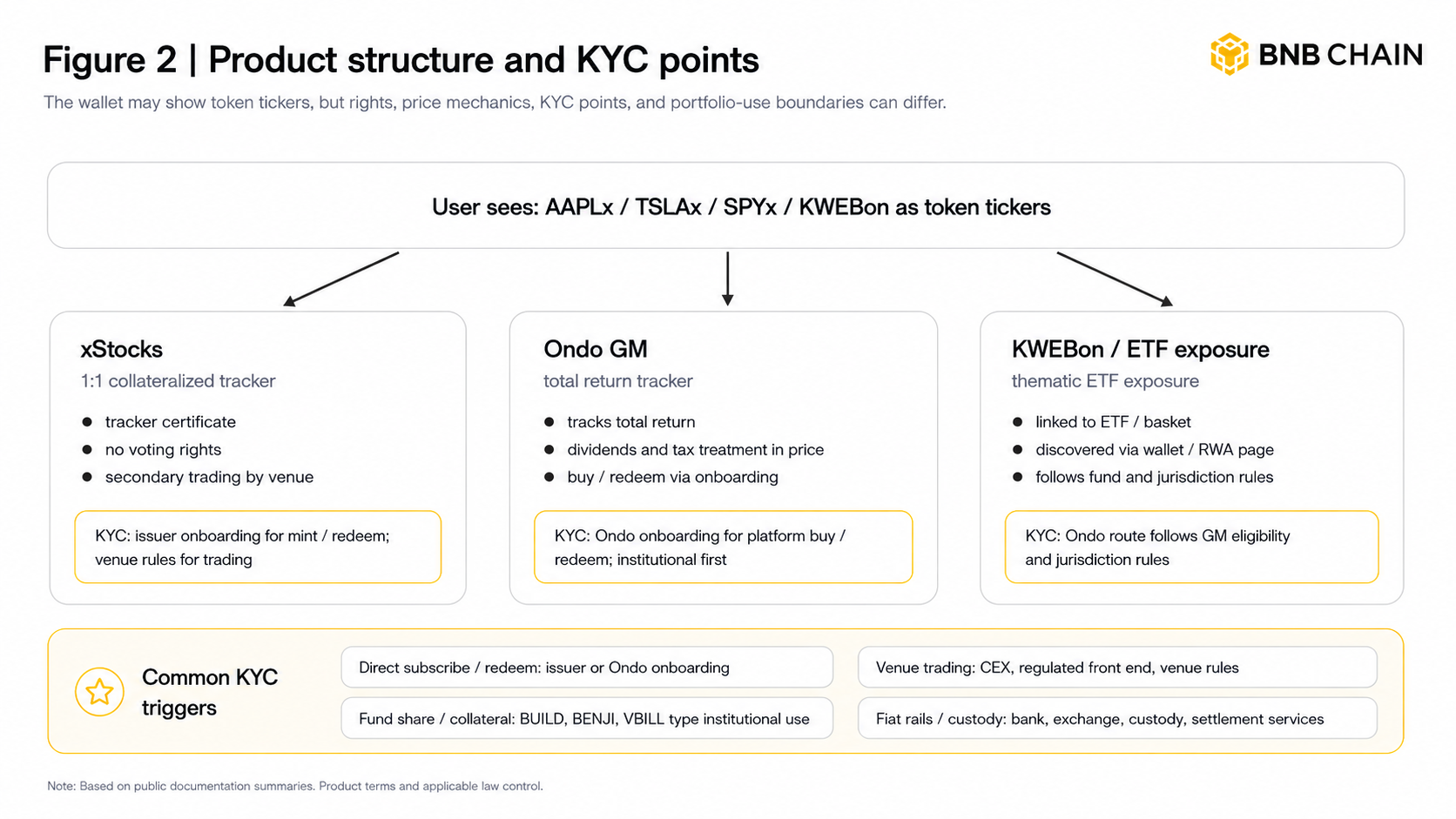

Product structures differ

Users receive an onchain form of stock or ETF exposure. The underlying securities are connected through issuance, custody, and product terms. Those terms decide whether a token corresponds to one share or a basket of assets, whether voting rights pass through, how dividends and stock splits are handled, when issuance or redemption can happen, and whether the asset can enter DEXs, lending markets, or portfolio tools.

According to xStocks Documentation and FAQ, xStocks describes its products as 1:1 collateralized tokenized representations. The user receives a tracker certificate and does not receive shareholder voting rights. Secondary markets can trade 24/7 on supported platforms, while issuance and redemption generally operate around US market hours on a 24/5 basis.

KYC is not handled uniformly at the token layer. xStocks says the token itself is permissionless and transferable onchain. KYC is mainly completed by the platform or venue during user onboarding. If a user deals directly with the issuer for minting or redemption, KYC requirements and minimum transaction thresholds apply.

Ondo Global Markets uses a different structure. Ondo Docs define GM assets as total return trackers. The token price tracks the total return of the underlying asset, including reinvested dividends and withholding tax treatment. One token therefore does not necessarily equal the value of one share. Ondo also discloses daily attestations, overcollateralization, and a third-party security agent arrangement.

KYC sits closer to the platform itself. Buying, selling, or redeeming directly through Ondo GM requires Ondo onboarding. According to Ondo's Onboarding & KYC page, onboarding is currently open to institutional participants, while individual and retail onboarding is still pending. The Eligibility page also lists prohibited jurisdictions including the US and Canada, and sets professional or qualified investor requirements for certain regions.

Whether a tokenized asset needs KYC cannot be determined from the ticker alone. It depends on how the user enters the asset and what action the user takes. Secondary market trading, direct subscription and redemption, custody and settlement, fiat on and off ramps, and collateral use can each trigger different access rules.

Direct subscription or redemption usually requires issuer or platform onboarding. Trading through a CEX, custody account, or regulated front end follows the relevant venue's user access rules. BUIDL, BENJI, and VBILL are tokenized money market or Treasury fund shares that are generally designed for institutional or qualified clients, and their use as collateral is also subject to platform rules. Stablecoin transfers can be more open at the chain level, but fiat rails, exchange accounts, custody, and settlement still trigger KYC. For KWEBon, because it sits inside the Ondo framework, user eligibility mainly follows Ondo GM onboarding, eligibility, and jurisdictional restrictions.

Figure 2: Product structure and KYC points. The wallet may show several token tickers, but their rights, price mechanics, KYC points, and portfolio-use boundaries can differ.

These products may all look like tokens in a wallet. Once they enter DeFi, the differences show up in parameters. Lending markets need collateral ratios. Perps need oracles. DEXs have to deal with after-hours and weekend pricing, and liquidation systems need to handle price updates when the underlying securities market is closed. If a token has different dividend treatment, redemption windows, price convergence mechanics, or eligible trading regions, the same market move can turn into different slippage, discounts, margin requirements, or liquidation risk. DeFi brings product structure into automated rules.

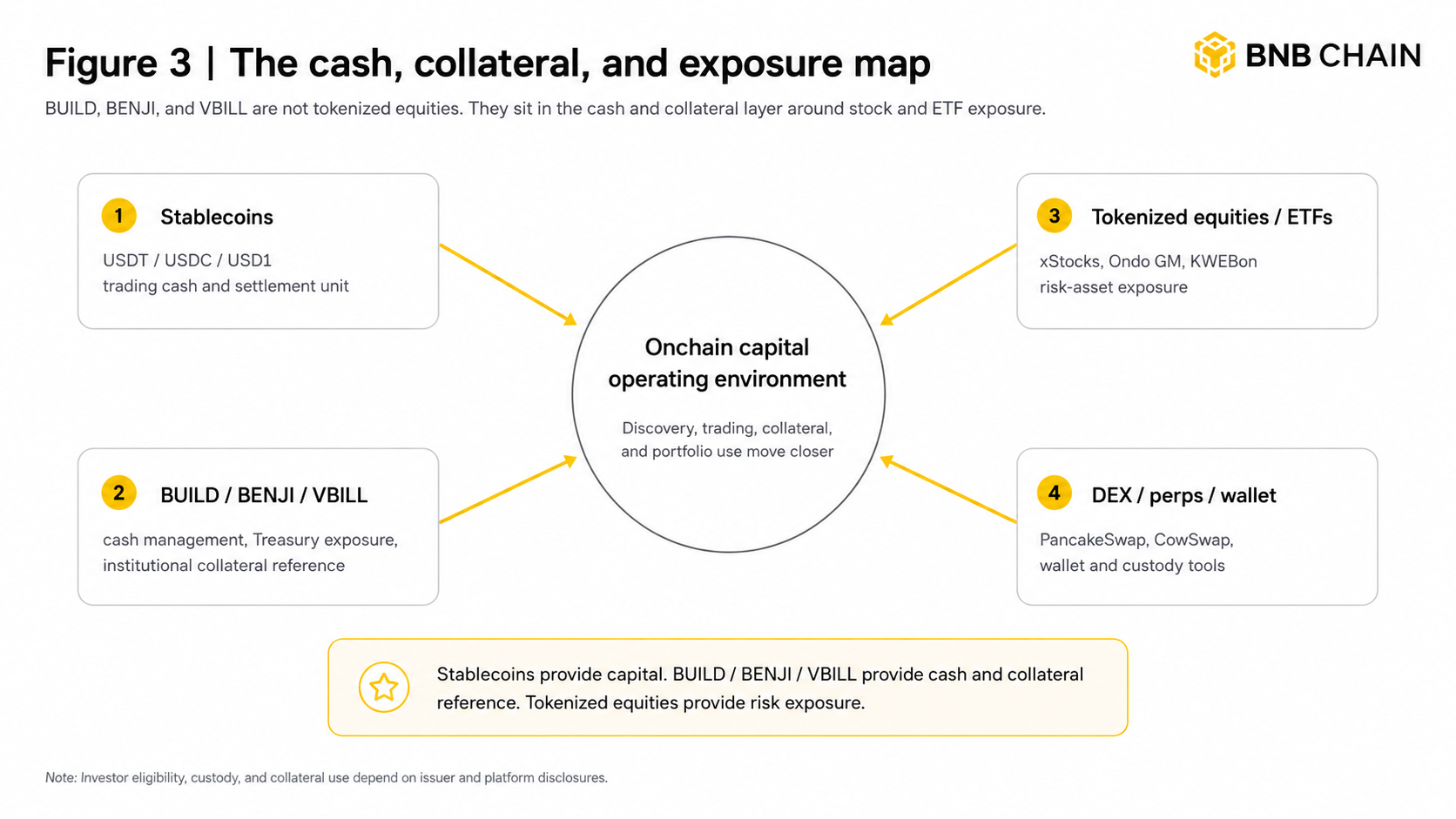

The cash and collateral layer: where BUIDL, BENJI, and VBILL fit

BlackRock BUIDL, Franklin Templeton Benji, and VanEck VBILL are adjacent RWA assets rather than tokenized equities. BUIDL is a tokenized money market fund, BENJI corresponds to Franklin Templeton's onchain fund share system, and VBILL is VanEck's tokenized US Treasury fund issued through Securitize.

All three sit in the funding and collateral layer. For tokenized equities to move from tradable tickers into assets that a funding system can use, the market needs more than stock and ETF exposure. It also needs stablecoins, cash management assets, and collateral that can support trading.

Figure 3: The cash, collateral, and exposure map. BUIDL, BENJI, and VBILL are not tokenized equities. They matter because they sit in the cash and collateral layer around tokenized stock and ETF exposure.

BNB Chain disclosed in its BUIDL announcement that BlackRock USD Institutional Digital Liquidity Fund, or BUIDL, launched on BNB Chain through Securitize and Wormhole, and was accepted by Binance as institutional off-exchange collateral.

Franklin Templeton's Benji has also integrated BNB Chain. BNB Chain disclosed the integration in its Benji Technology Platform announcement. Franklin Templeton later said in a 2026-02-11 announcement that eligible institutional clients could use Benji-issued tokenized money market fund shares as off-exchange collateral for Binance trading.

VBILL shows that Securitize's issuance infrastructure is not tied to one asset manager. In the Securitize / VanEck VBILL use case, BNB Chain described VBILL as VanEck's tokenized US Treasury fund available to qualified investors.

Without this layer, tokenized equities look more like tradable tickers. With it, stock and ETF exposure can start to fit into a fuller capital operating flow.

Trading capacity matters more than tokenized equity listings

Onchain data should be read through trading capacity. Asset deployment shows that an issuer has completed integration. Trading volume, routing, holder addresses, and TVL are closer to whether users and capital are actually entering the market.

TVL measures closer to asset deposits while DEX volume reflects trading capacity, and they do not always concentrate on the same chain.

As of 2026-05-12, the DefiLlama Ondo Global Markets page showed $985.72M in total value locked, with $484.11M on Ethereum, $473.18M on BSC, and $28.43M on Solana. The same page showed $958.56M in 30-day DEX volume, including $783.27M on BSC and $175.29M on Ethereum. Cumulative DEX volume was $5.609B, including $4.257B on BSC and $1.351B on Ethereum.

These figures describe trading capacity. Under DefiLlama's Ondo GM methodology, BSC has moved from an asset deployment venue into an observable trading environment.

xStocks gives another angle. In its 2026-04-30 announcement, xStocks said total transaction volume was close to $30B, onchain related scale had passed $5B, and unique onchain holders had passed 100,000. Now that xStocks is live on BNB Chain, the next data points to watch are whether BNB Chain develops sustained single-chain volume, holder addresses, DEX depth, and collateral use.

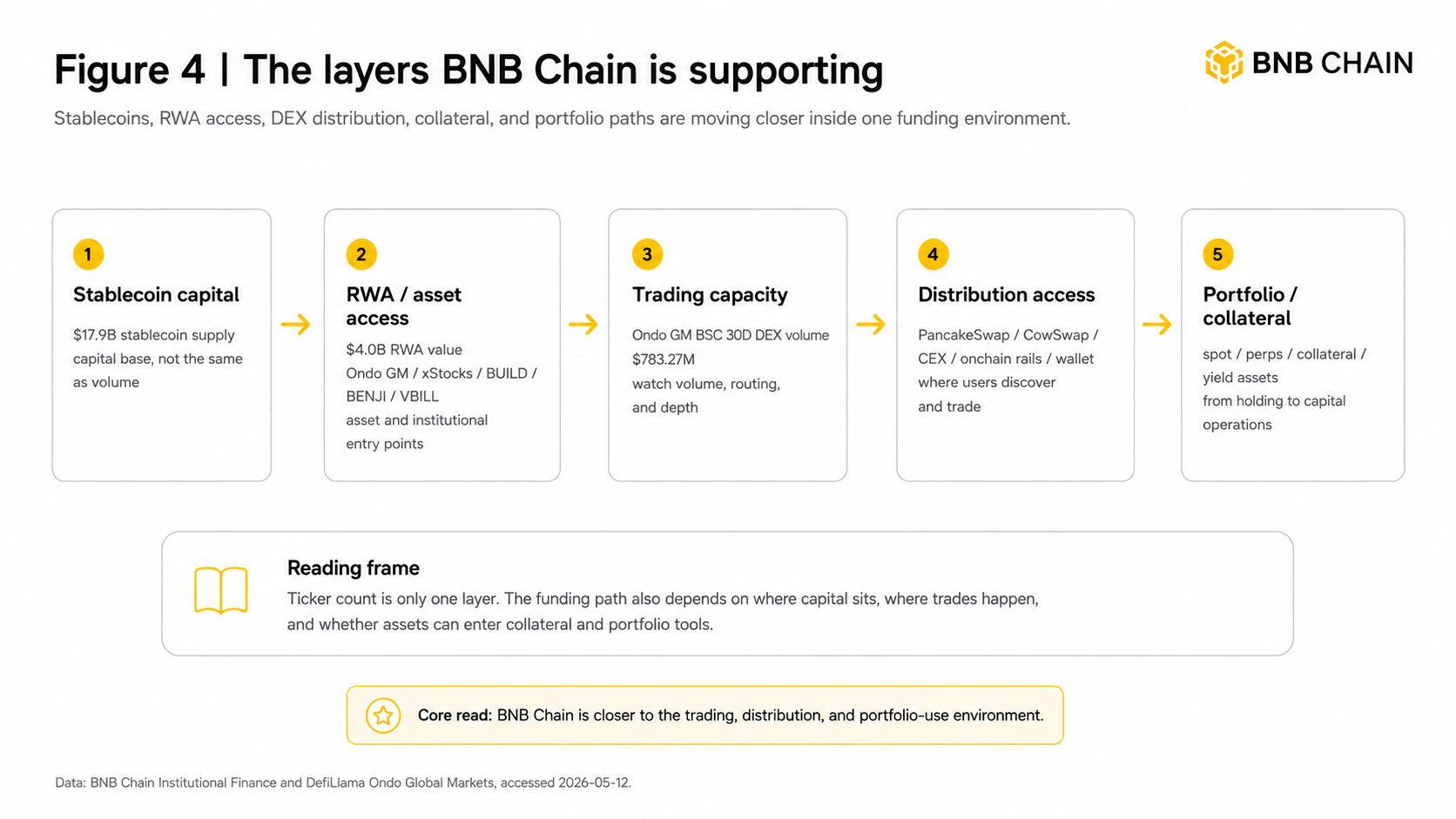

What BNB Chain is supporting

BNB Chain's role can be broken down by layer: asset issuance, asset discovery, funding source, trade execution, collateral, portfolio use, and compliance boundaries. In this context, it is closer to a trading, distribution, and portfolio-use environment.

Figure 4: The layers BNB Chain is supporting. Stablecoins, RWA asset access, DEX distribution, collateral, and portfolio paths are moving closer inside the same funding environment.

PancakeSwap is one connector. It is one of the spot entry points for Ondo and xStocks on BNB Chain, and it has also listed AAPL, AMZN, and TSLA stock perpetuals. When spot and derivatives sit on the same chain, users can hold tokenized equities and use perps for directional expression or risk management.

BNB Chain's infrastructure role maps to a funding path. Stablecoins supply the capital base, while Ondo and xStocks bring stock and ETF exposure. PancakeSwap and CowSwap handle trading, and BUIDL, BENJI, and VBILL sit in the institutional collateral layer. Each layer has boundaries, but they are starting to appear inside the same onchain funding environment.

Conclusion

The near-term expansion is asset breadth. xStocks has committed to 100+ additional stocks and ETFs beyond the 50+ already live on BNB Chain, and 1inch routing is in the pipeline. Ondo GM's retail onboarding remains pending; when it opens, pricing dynamics and liquidity for assets like KWEBon will shift. The more direct test is whether tokenized equities can enter lending markets and margin systems the way BUIDL and BENJI have for institutional off-exchange collateral.

Putting assets onchain was the simpler problem. What remains is building the infrastructure that makes them usable once they are there. The ticker is just the entry point.

Disclaimer

This article is for informational and ecosystem research purposes only. It does not constitute investment, legal, or financial advice. References to third-party projects, market data, and external platforms are based on publicly available information, and such data may change over time. Readers should assess their own risk and comply with the applicable laws and regulations of their jurisdiction before participating in tokenized equities, RWA, onchain trading, or other digital asset-related activities.

References

• RWA.xyz Global Market Overview

• BNB Chain Institutional Finance

• xStocks Is Now Live on BNB Chain with 50+ Tokenized Equities, with 100+ More Coming Soon,

• xStocks Launches on BNB Chain,

• DefiLlama: Ondo Global Markets,

• KraneShares CSI China Internet ETF - KWEB,

• xStocks Documentation、xStocks FAQ and xStocks Product Legal Overview

• Ondo Global Markets Documentation、Onboarding & KYC、Eligibility and Legal & Regulatory

• Franklin Templeton’s Benji Technology Platform Onboards BNB Chain

• Use Case: Securitize and VanEck Bring VBILL On-Chain To Unlock Tokenized Treasuries on BNB Chain